Commentary from Clean EDGE Asia

Green Grids: India’s Pathways and Asia’s Preparedness

Payal Dey examines India’s ambitious efforts to integrate renewable energy into its energy mix and explores the prospects for international grid integration to support the energy transition across Asia.

In 2013, India published a roadmap for the integration of renewables, along with corresponding assessments by the Central Electricity Authority (CEA), in its twelfth and final five-year plan.[1] In 2014, the plan-based approach was abandoned in favor of “cooperative federalism,” which included changes to the public financing mechanisms distributed between the central and state governments affecting the power sector. Despite an ambitious target for the energy mix, the portion of renewable energy (RE) sources in total power generation for the fiscal year 2012–13 was only 5%.[2] This increased to 20% in May 2023.[3] During the 28th Conference of the Parties (COP28), a global commitment was made to triple renewables by 2030 from the existing target of 2.5 times under ongoing policies and market structures.[4]

Against the backdrop of these policies, this essay focuses on India’s strategic positioning in Asia for integrating RE after the country attained nearly complete electrification in 2018 and for aiding the commitment toward panchamrit (five nectars) announced at COP26 in Glasgow.[5] The essay explores the prospects for international grid integration to support more RE and considers bilateral and multilateral steps to navigate the geopolitics of several policies and programs in Asia.

The Greening of the Grid Program

In 2015, India set an ambitious target of achieving 175 gigawatts (GW) of RE by 2022 as one of its intended nationally determined contributions under the United Nations Framework Convention on Climate Change (UNFCC).[6] This target included 100 GW of solar, 60 GW of wind, 10 GW of bioenergy, and 5 GW of small hydro, which required advanced weather and power system modeling through multi-institutional studies for suitable grid integration.[7] During a meeting between Prime Minister Narendra Modi and President Barack Obama, the United States offered capacity building for monitoring and reporting of the climate pledges.[8]

India presented even more aggressive goals in its national statement at COP26. Out of the five nationally determined contributions (panchamrit), two were more pronounced targets on renewable energy: attaining 500 GW by 2030 and meeting 50% energy demand through RE.[9] Building a grid dominated by renewables to achieve a net-zero target for 2070 poses challenges for managing the intermittency of RE generation. India’s intense climate action under the UNFCC thus has the potential to direct both investments and technologies for a clean and climate resilient transition.

The Greening the Grid (GTG) program was a five-year initiative co-led by India’s Ministry of Power and the U.S. Agency for International Development (USAID) under the U.S.-India Strategic Clean Energy Partnership, along with the World Bank’s Energy Sector Management Assistance Program, the U.S. Department of Energy, the U.S. Department of State, and the 21st Century Power Partnership. It was institutionalized by the National Renewable Energy Laboratory (NREL) and the Joint Institute for Strategic Energy Alliances to liaison with partners and stakeholders like the Clean Energy Ministerial and the United Nations.[10] GTG was a focused program implemented under the Renewable Integration and Sustainable Initiative (RISE) by USAID in India and the Asia EDGE (Enhancing Development and Growth through Energy) initiative to support India’s large-scale integration of RE into the main grid.[11] The performance evaluation of GTG that was concluded in July 2021 reported limited success due to design and implementation issues, coupled with delays due to the pandemic.[12]

India’s Priorities for Integrating Renewables into the Grid

Electrification has been a key priority for India since independence, yet it only achieved close to 100% electricity access in 2018, when the last 100 million households were connected to the main grid. The next essential step to household grid connectivity was providing people with affordable, reliable, and clean energy.[13] While the RE targets were set by the government, the GTG project included developing a robust cost and production model that optimized scheduling and dispatch of generation, taking into consideration market, operational, and physical constraints.[14] The key objectives of GTG were developed by core members that included subsidiaries of India’s Ministry of Power; the national grid operator, Power System Operation Corporation Ltd. (POSOCO), the state load dispatch centers in the western region (Maharashtra, Gujarat, and Rajasthan) and southern region (Tamil Nadu, Karnataka, and Andhra Pradesh); the central transmission utility, Power Grid Corporation of India (POWERGRID); the CEA; the NREL; and Lawrence Berkeley National Laboratory. With state-of-the-art planning tools, the agencies were collectively able to utilize high-resolution RE data for cost savings, optimal utilization, transmission, stability during contingencies, and efficient investment recoveries through affordable tariff rates.

The priorities for enabling, designing, and stabilizing the integration of RE into the national grid were also addressed in the Green Energy Corridor project, led by POWERGRID under the Ministry of New and Renewable Energy, to facilitate intrastate and interstate absorption and transmission of RE.[15] Commissioned in 2012 and financed by the Asian Development Bank in 2015, the Green Energy Corridor laid the foundation for carrying out more projects for enriching India’s power grid with renewables.

Low RE generation is mainly due to curtailment, where wind or solar generation exceeds the demand at peak production times and operators must throttle these sources down. The GTG studies undertaken by India and the United States in 2017 presented modeling frameworks through a national study that was subsequently validated through regional studies to coordinate operations among states for reducing this curtailment. Since then, both the International Energy Agency (IEA) and NITI Aayog have conducted a series of workshops at the state, regional, and national levels to accelerate RE into the grid system. Since 2020, both NITI Aayog and IEA, along with the British High Commission, have been sensitizing state governments through workshops on the transformation of the power system. India, being the world’s largest synchronous grid since 2014, identified building a dedicated transmission network for integrating higher variable renewable Energy (VRE), using both wind and solar.[16] This would necessitate requirements for power system flexibility, particularly on the supply side, that could be met by installing batteries and pumped storage hydropower plants—the demand for which is estimated to increase by over 30 times (nearly 27 GW) and 1.5 times (close to 10 GW), respectively, from 2019 to 2030.[17]

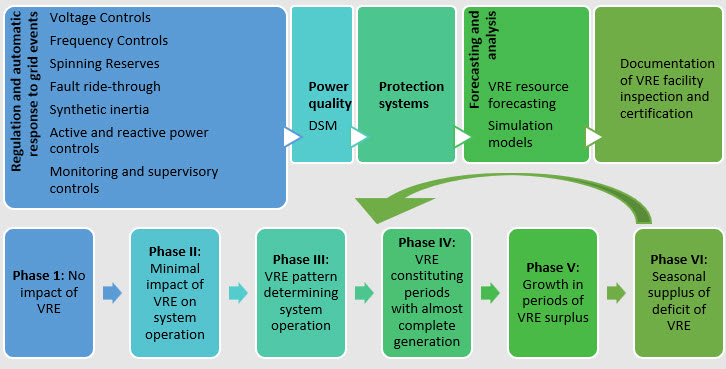

The main objective of power system operations is to keep the supply balanced with the demand—i.e., power quality and frequency stability in the short run, and constant production and transmission loads in the long run. The integration of VRE into the bulk power system requires an additional set of interconnection procedures and standards.[18] The most basic of these are illustrated in Figure 1. Challenges to integration include the concentration of RE within states, which creates problems for interstate transmission and demand-side management; the lack of real-time RE data, which makes long-term demand projections unreliable; evolving regulatory frameworks for renumerating demand response; RE curtailment; the financial stability of distribution companies due to long-term contracts with coal plants; and grid codes. All these factors create market inefficiencies, resulting in higher consumer tariffs.[19] The technical standards are designed for overcoming the challenges at each phase in the process.

Figure 1: Requirements for VRE integration into power grids

Source: World Bank, “Grid Integration Requirements for VRE—Technical Guide,” Energy Sector Management Assistance Program, July 2019; and IEA and NITI Aayog, “Renewables Integration in India,” June 2021, 26.

Current Status of Renewables and Integration Preparedness

India attained 95% of the enhanced target of 175 GW of RE by December 2022.[20] This included 46.85 GW of large hydropower projects that were added to the definition of RE only in 2019.[21] The Ministry of New and Renewable Energy had sought an extension of seven and a half months due to the Covid-19 pandemic.[22] As of January 2024, nearly 182 GW of RE had been installed, including approximately 74 GW of solar, 45 GW of wind, 11 GW of bioenergy, and 5 GW of small hydro. While India has met its targets for bioenergy and small hydro, the shortfalls of solar and wind installation capacity are 26% and 25%, respectively.[23] Further, India has pledged that by 2030, 500 GW of the total installed capacity would be from non–fossil fuel sources (RE and nuclear). To attain this goal, it would invite 50 GW of bids for five consecutive fiscal years starting with 2023–24.[24]

Until February 2023, around 80 GW of RE were in various stages of implementation, with 40 GW in the bidding process through government-notified renewable energy implementing agencies.[25] Considering that RE projects take around 18–24 months for commissioning, upgrading, adding, and evacuating, 500 GW of RE from non–fossil fuel sources of energy seems achievable. POSOCO, which manages India’s grid operations and integration, has emphasized the importance of technology deployment while building capacity across all stakeholders. The specific steps recommended by POSOCO for preparing the electricity grid for RE by 2030 are forward-looking grid codes and technical standards for the use of inverter-based resources as retrofits for new grid aspects, ensuring resource adequacy to counter the intermittent nature of RE sources, increasing the flexibility of conventional generation to avoid grid instability from the variability of renewables, and catering to bidirectional power flows through flexible alternating current (AC) and high-voltage direct current (DC).[26] The progress and preparedness of integrating RE into the grid could be corroborated with the findings of the Lawrence Berkeley National Laboratory. Options include cross-seasonal support from large hydro projects, use of state-of-the-art forecasting techniques for real-time data, and the creation of robust intraday and ancillary services markets.[27] The new grid code for 2023 contributes to preparedness for integration and applies to users, dispatch centers, transmission utilities, power committees, exchanges, and agencies of the entire country. It contains extensive provisions for integration of VREs, such as performance monitoring, scheduling, dispatch criteria, ancillary services, reserves, and cybersecurity.[28]

Phases of Grid Integration and Subnational Progress

State governments currently own around 30% of power generation, the central government owns around 25%, and the private sector owns the remaining 45%. The ten renewables-rich states have a higher share of VRE than most countries in the world, contributing almost 97% of India’s RE generation from solar and wind. Out of these ten, the annual average electricity generation of the top four states—Gujarat (14%), Tamil Nadu (18%), Rajasthan (20%), and Karnataka (29%)—is higher than the national average of 8.2%. In 2020–21, these four states, along with Telangana, were already in Phase III (out of six phases) of grid integration. In this phase, RE determines the operation pattern of the power system and is facing system integration challenges, such as exporting power to other states, displacing thermal power plants with RE, and curtailing RE for system security. These phases, as defined by the IEA, are illustrated in Figure 1. Phase IV constitutes generation with a major share of VRE. Since only a few countries have reached this phase, both Phases V and VI could be considered as extensions of Phase IV. Out of the top four VRE states in India, Karnataka, Rajasthan, and Tamil Nadu are fast approaching this phase.

The IEA developed two models for production—the India Regional Model and the Gujarat State Model—to undertake a techno-economic analysis for a one-year assessment of 2030, with 2019 as the base year. These power system models were like the studies done in the GTG report. However, whereas the IEA models used hourly time resolution, the GTG studies used 15-minute weather profiles from the NREL’s database. The GTG national study had identified several characteristics for an optimum model: responsibility for scheduling and dispatching, balanced treatment of central and state-level generation units, interconnection of RE to both interstate and intrastate lines, must-run status for RE, and adequate reserve requirements.[29] Reflecting a more practical view, the IEA’s Gujarat State Model is based on historical demand, taking into consideration agriculture, “contracted capacities” both within and outside the state, and flexibility options with the Gujarat government and other stakeholders. It further reflects a reduction in CO2 emissions and curtailment to 1% and 6%, respectively, by 2030, compared with 4% and 5% in the India Regional Model.[30]

Geopolitics of Green Grid Integration in Asia

As part of an initiative to develop a transnational grid, India proposed the idea of One Sun, One World, One Grid (OSOWOG) for interconnecting solar energy around the globe at the first assembly of the International Solar Alliance (ISA) in 2018. Subsequently, at COP26 India’s OSOWOG vision was joined by the United Kingdom’s Green Grids Initiative (GGI) and the World Bank’s Sustainable Partnership for Rooftop Acceleration to connect 140 countries with new infrastructure for the provision of affordable solar energy across borders.[31] The ISA aims to drive interconnectivity across the Middle East, South Asia, and Southeast Asia in the first phase; across Africa in the second; and globally in the final phase through an investment of $1 trillion for developing countries until 2030.

A similar project is the $16 billion Australia-Asia Power Link to connect northern Australia with large solar resources in Southeast Asia that boast significant geothermal, hydropower, wind, bioenergy, and ocean reserves.[32] Although the project was eventually found to be unfeasible due to huge investment costs in building subsea cables and rising costs of raw materials, coupled with geopolitical turbulence in Southeast Asia, alternative pathways to grid integration across regions have emerged, such as the trade of critical minerals like cobalt, lithium, and vanadium from Australia for bauxite, nickel, and rare earth elements from Southeast Asia. Other possibilities are resolving energy transition bottlenecks in Southeast Asia through technology transfers and facilitating the direct participation of Australian firms in the regional markets through low-cost financing.[33]

Among the benefits of regional integration could be greater energy security and more efficient energy markets, resulting in economies of scale and price convergence. The Bay of Bengal Initiative for Multi-Sectoral Technical and Economic Cooperation (BIMSTEC), comprising Bangladesh, Bhutan, India, Myanmar, Nepal, Sri Lanka, and Thailand, is a crucial step. Member countries have signed a memorandum of understanding for grid integration subject to relevant laws for cross-border power flows through operational harmonization. There is also an opportunity for the BBIN Initiative, comprising Bangladesh, Bhutan, India, and Nepal, to use existing infrastructure, such as the Green Energy Corridor, for tapping hydropower potential at the bilateral level due to seasonal variations in the demand patterns of these countries.[34] Additionally, the 39th ASEAN Ministers on Energy Meeting in 2021 paved the way for multilateral power trade and RE integration into the ASEAN Power Grid with the help of the International Renewable Energy Agency. Under OSOWOG, India plans to connect its national grid with Myanmar and Thailand and has already engaged a firm to address key challenges such as pricing, regulatory frameworks, and financing.

The Way Forward

India is playing a crucial role in combatting climate change. Following its G-20 presidency in 2023, the country’s leadership in the global energy transition is even more pronounced. The concluding Energy Transitions Ministerial Meeting shared twenty outcomes that highlighted a vision for interconnected grids and regional power systems integration through “ambition, transition, and transmission.”

This objective of greater energy interconnection and trade is shared by the ASEAN power grid through multi-energy complementation and solutions to seasonal variation by connecting the grid to both China and South Asia by 2050. The GTG studies by the NREL have further highlighted the potential of India establishing a high-voltage DC connection with Sri Lanka and increasing energy trade with Nepal. In addition, the Green Grids Initiative has been endorsed by nearly 90 countries. The GGI estimates that $21.4 trillion in investment will be required to power the grids with RE by 2050.[35] This target could be met through public-private partnerships, with the private sector investing in low-cost capital and with governments providing a safe regulatory environment. Successful cases in Europe and ASEAN countries are paving the way for ambitious multilateral and multidirectional actions to ensure progress toward the broad goals of “greening the grid.” These goals are energy security, sustainable development, and decarbonization, which are also the objectives of the EDGE program.

Payal Dey is currently an independent public policy and energy researcher based out of New Delhi. She was a 2022–23 Clean EDGE Asia Fellow.

Endnotes

[1] Central Electric Authority (India), “Large Scale Grid Integration of Renewable Energy Sources—Way Forward,” November 2033.

[3] Ministry of Power (India), “Broad Overview of the Monthly Renewable Energy Generation,” Renewable Project Monitoring Division, April 2023.

[4] International Energy Agency (IEA), “Massive Expansion of Renewable Power Opens Door to Achieving Global Tripling Goal Set at COP28,” January 11, 2024, https://www.iea.org/news/massive-expansion-of-renewable-power-opens-door-to-achieving-global-tripling-goal-set-at-cop28.

[5] “Cabinet Approves India’s Updated Nationally Determined Contributions to Be Communicated to the UNFCC,” Press Information Bureau (India), August 3, 2022, https://pib.gov.in/PressReleasePage.aspx?PRID=1847813. For more details on panchamrit, see “Panchamrit—a Striding Step towards Achieving India’s Goal of Net Zero by 2070,” Impact and Policy Research Institute, September 1, 2023, https://www.impriindia.com/insights/panchamrit-india-net-zero.

[6] “Year End Review—MNRE,” Press Information Bureau (India), December 15, 2015, https://pib.gov.in/newsite/printrelease.aspx?relid=133220.

[7] “Greening the Grid: Pathways to Integrate 175 Gigawatts of Renewable Energy into India’s Electric Grid,” National Renewable Energy Laboratory, April 2017, https://sarepenergy.net/wp-content/uploads/2022/10/NREL-Factsheet-on-National-report-Pathways.pdf.

[8] Anand Gupta, “U.S. Hails PM Modi’s ‘Enormously Impressive’ Renewable Pledge,” EQ International, December 3, 2015, https://www.eqmagpro.com/us-hails-pm-modis-enormously-impressive-renewable-pledge.

[9] “Panchamrit—a Striding Step towards Achieving India’s Goal of Net Zero by 2070.”

[10] David Palchak et al., “Greening the Grid: Pathways to Integrate 175 Gigawatts of Renewable Energy into India’s Electric Grid,” National Renewable Energy Laboratory, 2017, http://www.nrel.gov/docs/fy17osti/68530.pdf.

[11] USAID and Government of India, Electric Vehicle Charging Infrastructure and Impacts on Distribution Network (New Delhi, June 2020), https://sarepenergy.net/wp-content/uploads/2022/10/EV-White-paper-Revised-13-07-2020.pdf.

[12] Amit Bando et al., “USAID/India Greening the Grid (GTG) Project—Final Performance Evaluation,” USAID, October 13, 2021, https://pdf.usaid.gov/pdf_docs/PA00Z6ZH.pdf.

[13] IEA and NITI Aayog, “Renewables Integration in India,” June 2021, https://iea.blob.core.windows.net/assets/7b6bf9e6-4d69-466c-8069-bdd26b3e9ed1/RenewablesIntegrationinIndia2021.pdf.

[14] Palchak et al., “Greening the Grid.”

[15] Asian Development Bank, “Power Grid Corporation of India Limited Green Energy Corridor and Grid Strengthening Project (India),” Extended Annual Review Report, November 2022, https://www.adb.org/sites/default/files/project-documents/44426/44426-018-xarr-en.pdf.

[16] IEA and NITI Aayog, “Renewables Integration in India.”

[17] CEA, “Report on Optimal Generation Capacity Mix for 2029–30,” April 2023, https://cea.nic.in/wp-content/uploads/irp/2023/05/Optimal_mix_report__2029_30_Version_2.0__For_Uploading.pdf.

[18] World Bank, “Grid Integration Requirements for VRE—Technical Guide,” Energy Sector Management Assistance Program, July 2019, https://documents1.worldbank.org/curated/pt/934921562859528380/pdf/Grid-Integration-Requirements-for-Variable-Renewable-Energy.pdf

[19] Palchak et al., “Greening the Grid.”

[20] “Year End Review—MNRE,” Press Information Bureau (India), December 20, 2022, https://pib.gov.in/PressReleasePage.aspx?PRID=1885147.

[21] Divyani Dubey, “Status Check: Has India Achieved Its Goal of 175 GW Renewable Energy by 2022?” Fact Checker, December 30, 2022, https://www.factchecker.in/context-check/status-check-has-india-achieved-its-goal-of-175-gw-renewable-energy-by-2022-847822.

[22] Lok Sabha Secretariat, “Twenty-Eighth Report,” Standing Committee on Energy (2021–22), July 2022, https://eparlib.nic.in/bitstream/123456789/931975/1/17_Energy_28.pdf.

[23] CEA, “Installed Capacity Report,” March 2024, https://cea.nic.in/installed-capacity-report/?lang=en.

[24] “Government Declares Plans to Add 50 GW of RE Annually for Next 5 Years to Achieve the Target of 500 GW by 2030,” Press Information Bureau (India), April 5, 2023, https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1913789.

[25] The Solar Energy Corporation of India Ltd., NTPC Ltd., NHPC Ltd., and SJVN Ltd., which is a public sector enterprise under the government of India, are designated as renewable energy implementing agencies for calling bids.

[26] “Interview with S.R. Narasimhan,” Power Line, September 2022, https://posoco.in/wp-content/uploads/2022/10/CMD-Interview-with-Power-Line-Magazine.pdf.

[27] Amol Phadke, Nikit Abhyankar, and Ranjit Deshmukh, “Techno-Economic Assessment of Integrating 175GW of Renewable Energy into the Indian Grid by 2022,” Lawrence Berkeley National Laboratory, Energy Analysis and Environmental Impacts Division, December 2016, https://eta-publications.lbl.gov/sites/default/files/pdf_6.pdf.

[28] “CERC Notifies Indian Electricity Grid Code Regulation, 2023,” Power Line, May 2023, https://powerline.net.in/2023/05/30/cerc-notifies-cerc-indian-electricity-grid-code-regulations-2023.

[29] Palchak et al., “Greening the Grid.”

[30] Binit Das, “Renewable Energy Integration in India: Ways to Maximise Solar, Wind Power System,” DownToEarth, August 11, 2021, https://www.downtoearth.org.in/blog/energy/renewable-energy-integration-in-india-ways-to-maximise-solar-wind-power-system-78391.

[31] “World’s First Transnational Solar Panel Network GGI-OSOWOG Launched in Glasgow,” PR Newswire, November 2, 2021.

[32] Sustainable Partnership for Rooftop Solar Acceleration in Bharat (SUPRABHA), OSOWOG Newsletters, September 2020.

[32] Nicholas Basan, “Sun Cable’s Collapse and the Australian Role in Southeast Asia’s Energy Transition,” Diplomat, February 2, 2023, https://thediplomat.com/2023/02/sun-cables-collapse-and-the-australian-role-in-southeast-asias-energy-transition.

[34] Shafiqul Alam, “Cross-Border Electricity Trade among BBIN Countries Offers Mutual Benefits,” Institute for Energy Economics and Financial Analysis, February 28, 2023, https://ieefa.org/resources/cross-border-electricity-trade-among-bbin-countries-offers-mutual-benefits.

[35] “Green Grids Initiative,” Climate Parliament, https://www.climateparl.net/green-grids-initiative.